Oxford Economics has teamed up with Aon’s Global Construction and Infrastructure Group to publish a new global construction forecast report to 2037. It will map growth for the top 50 construction markets globally, at a time when climate change mitigation efforts drive up growth in key markets.

Scheduled to be published in the first quarter of 2023, the new report will give an overview of the health of the global economy and examine how rising populations and rapid urbanisation in emerging markets are expected to impact growth in key construction markets.

The report is sponsored by the largest and most well-known names in construction, according to Oxford Economics. It will identify the high-growth markets for construction and provide decision-makers in construction with a powerful resource for forward planning and strategy during a period of unprecedented uncertainty.

Continued shift to emerging markets

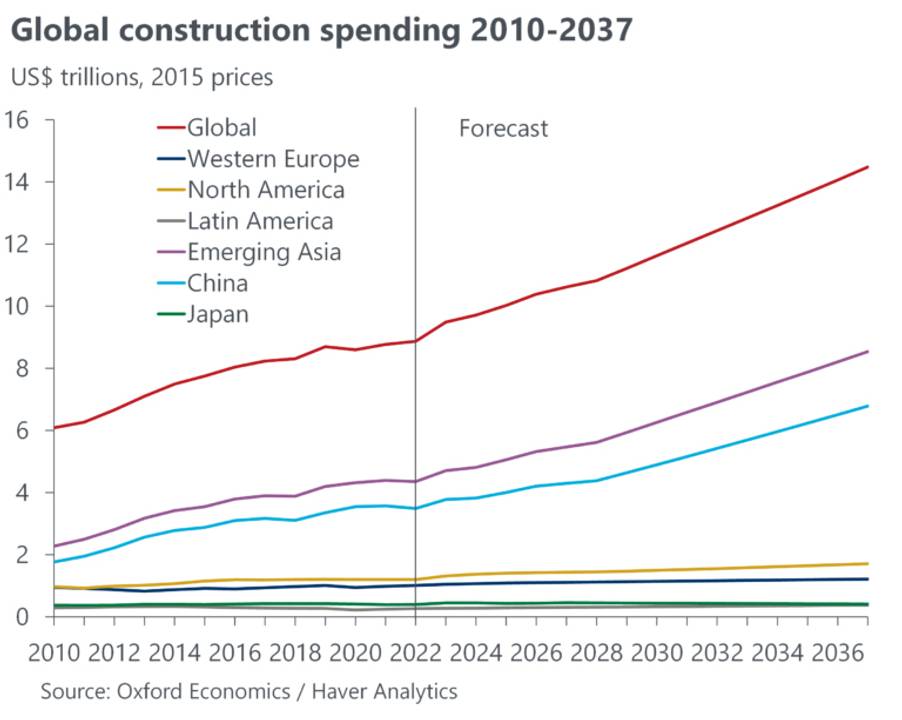

Growth of US$5.6 trillion in construction is expected over the 15-year period from 2022 to 2037 – representing a growth of over 60% in the size of the global construction market.

Construction will see a continued shift to emerging markets. The fastest-growing region globally is expected to be emerging Asia, growing by US$4.2 trillion to an US$8.5 trillion construction market by 2037.

India is expected to be the fastest-growing major construction market globally and will double its size from 2022 to 2037.

China is expected to contribute US$3.3 trillion of growth to the global construction market to 2037 – over 50% of global growth for construction. Growth in non-residential sectors such as healthcare and biotech will outstrip growth in infrastructure or housing as China’s economy transitions towards a market-led economy.

Rising populations and rapid urbanisation in emerging markets will be a key growth driver for construction. Global population is expected to rise by one billion people, from 7.9 billion in 2022 to 9.0 billion by 2037. Population growth and urbanisation will grow fastest across sub-Saharan Africa.

Latin America is expected to grow at the same pace as North America, while Western Europe and the developed economies of Asia Pacific are expected to be the slowest-growing regions.

The construction market in Japan is expected to remain the same size in 2037 as it was in 2022 with growth declining from 2028, as the population shrinks.

The climate challenge for construction will be its greatest opportunity. “The challenges of dealing with climate change will be a significant growth driver for construction globally and will create new industries and employment,” said Graham Robinson, global infrastructure and construction lead at Oxford Economics.

“With the built environment accounting for almost 40% of all greenhouse gas emissions globally, the transition to clean energy and new resilient infrastructure will boost growth for construction.”

Big potential in infrastructure

Climate change is arguably the greatest challenge for construction. The need to build resilient infrastructure and the race to achieve net zero by 2050 will mean huge programmes of infrastructure. Investment in the transition of energy grids to renewable sources of energy and transport networks towards green mobility will remain high growth markets as the US$1.2 trillion Infrastructure Plan in the US and €750 billion Next Generation EU promote growth and recovery from the pandemic.

Current inflationary pressures across economies are expected to largely dissipate starting in 2023 as the effects of an unprecedented surge in demand post-Covid normalise, and supply-chain disruptions are resolved. Headline inflation is not expected to return to pre-pandemic levels until late 2023 while persistent inflation for key construction materials and labour is likely to remain for longer, into the medium term, until supply chain disruptions ease.

With central banks firmly focused on bringing inflation down, the risk of a near-term recession has increased – a global recession is expected to be avoided, but contractions in GDP in both Europe and North America during 2023 are expected. The Eurozone looks particularly vulnerable to any further shocks as the Russia-Ukraine war continues and the German construction market is already experiencing a sizeable downturn this year.

“The use of technology to build the digital twins of real assets and the adoption of modern industrialised construction, will drive decarbonisation and improve productivity massively. The digitalisation of construction supports innovative risk management solutions as construction risks become more transparent and auditable,” said James MacNeal, global head of construction and infrastructure at Aon Global Infrastructure and Construction Group.

Image credits

Image 1: Danny Lau/Unsplash

Image 2: Oxford Economics/Haver Analytics